Which Of The Following Accounts Does A Manufacturing Company, But Not A Service Company, Have?

i.vii How Product Costs Menses through Accounts

Learning Objective

- Place how costs flow through the 3 inventory accounts and cost of goods sold account.

Question: Custom Furniture Company'southward directly materials include items such as wood and hardware. Straight labor involves the employees who build the custom tables. Manufacturing overhead includes items such equally indirect materials (glue, screws, nails, sandpaper, and stain), indirect labor (production supervisor), and other manufacturing costs, such as manufacturing plant equipment maintenance and factory utilities. What accounts are used to record the costs associated with these items, and where do these accounts appear in the fiscal statements?

Answer: All the costs mentioned previously for Custom Furniture are production costs (also chosen manufacturing costs). Product costs are recorded equally an asset on the balance sheet until the products are sold, at which betoken the costs are recorded as an expense on the income statement. To tape product costs as an asset, accountants use one of 3 inventory accounts: raw materials inventory, work-in-process inventory, or finished goods inventory. The account they utilise depends on the product's level of completion. They use one expense account—cost of goods sold—to tape the production costs when the appurtenances are sold.

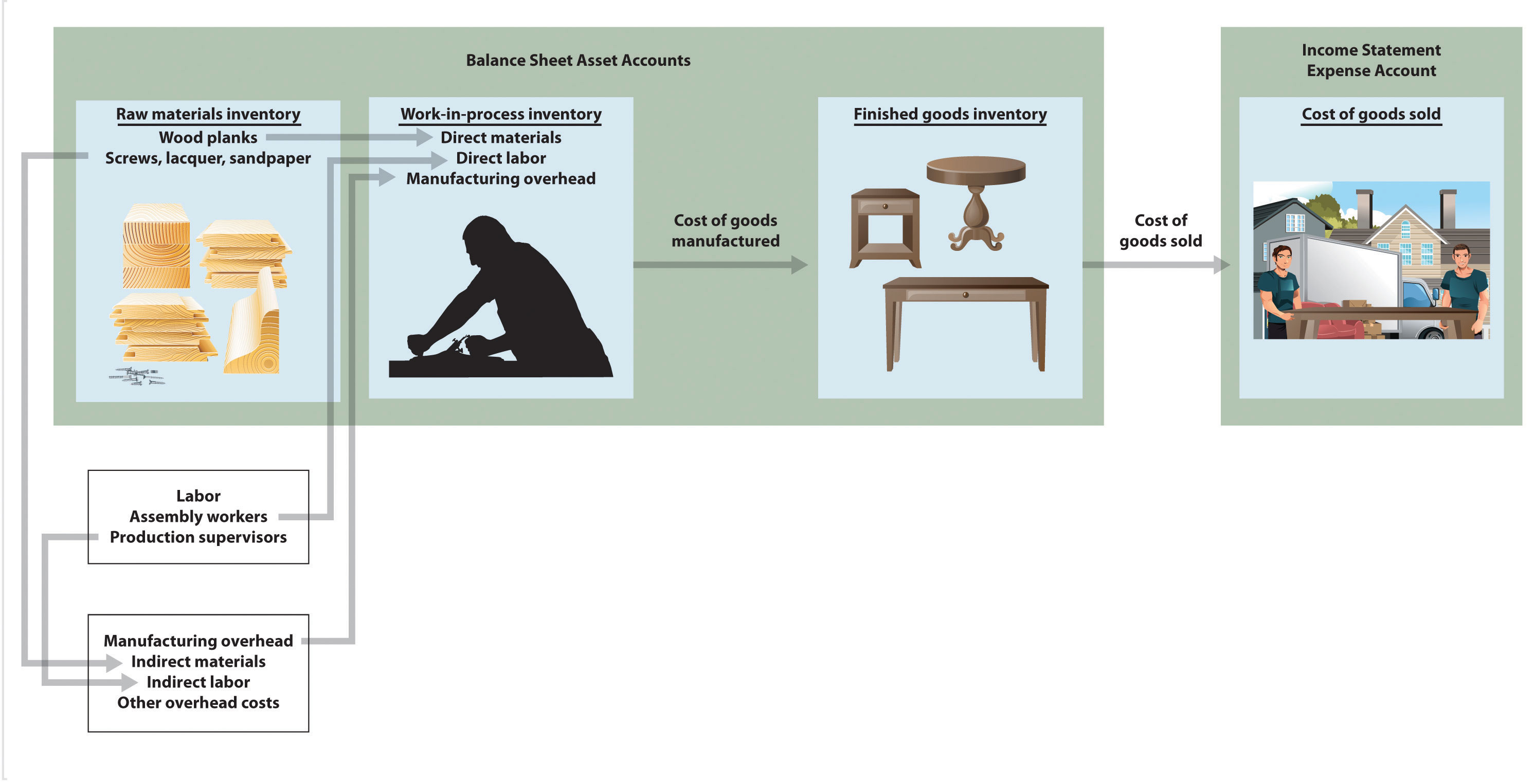

Table one.4 "Accounts Used to Tape Product Costs" summarizes the accounts used to track product costs. Figure 1.6 "Flow of Product Costs through Residuum Sail and Income Argument Accounts" shows how product costs flow through the remainder sheet and income statement. Lastly, Note 1.57 "Business concern in Action 1.7" provides an instance of how the accounts shown in Table ane.4 "Accounts Used to Record Product Costs" and Figure 1.6 "Flow of Product Costs through Balance Sail and Income Argument Accounts" appear in financial statements. Take fourth dimension to review these items carefully. Your understanding of them will aid clarify how product costs menstruation through the accounts and where product costs appear in the financial statements. The following word provides further description.

Production Costs on the Residue Sheet

Question: What is the deviation betwixt raw materials inventory, piece of work-in-procedure inventory, and finished goods inventory?

Answer: Each of these accounts is used to record production costs depending on where the production is in the product process, and each account is an asset account on the balance sheet.

Raw Materials

The raw materials inventoryAn account used to record the cost of materials not yet put into product. account records the toll of materials not yet put into production. For Custom Article of furniture Visitor, this account includes items such as wood, brackets, screws, nails, mucilage, lacquer, and sandpaper.

Work in Procedure

The piece of work-in-process (WIP) inventoryAn account used to record costs associated with products in the production process that are non yet complete. account records the costs of products that have not nevertheless been completed. Suppose Custom Furniture Company has eight tables that are all the same in production at the end of the year. All manufacturing costs associated with these incomplete eight tables—direct materials, direct labor, and manufacturing overhead—are included in the WIP inventory account.

One time appurtenances in WIP inventory are completed, they are transferred into finished goods inventory. The cost of completed goods that are transferred out of WIP inventory into finished appurtenances inventory is called the cost of goods manufacturedThe price of completed goods transferred from work-in-procedure inventory into finished goods inventory. .

Finished Goods

The finished goods inventoryAn account used to record the manufacturing costs associated with products that are completed and fix to sell. account records the manufacturing costs of products that are completed and ready to sell. Suppose Custom Article of furniture Company has v completed tables at the end of the yr (in addition to the 8 partially completed tables in piece of work-in-procedure inventory). The manufacturing costs of these v tables—directly materials, straight labor, and manufacturing overhead—are included in the finished goods inventory account until the tables are sold. (For the purposes of this case, presume the tables are "sold" when delivered to the customer.)

Product Costs on the Income Statement

Question: The costs of materials not even so put into production are included in raw materials inventory. The costs associated with products that are non notwithstanding complete are included in WIP inventory. And the costs associated with products that are completed and ready to sell are included in finished goods inventory. What happens to the production costs in finished goods inventory when the products are sold?

Respond: When completed goods are sold, their costs are transferred out of finished goods inventory into the price of appurtenances soldAn expense account on the income argument that represents the production costs for all goods sold during the period. business relationship. Cost of goods sold is an expense business relationship on the income argument that represents the product costs of all goods sold during the period.

For example, suppose Custom Furniture Company sells one tabular array that price $3,000 to produce (i.e., direct materials, direct labor, and manufacturing overhead costs incurred to produce the table total $iii,000). The $three,000 cost is in finished goods inventory until the entry is made to record the sale, at which time finished goods inventory is reduced past $3,000 (the table is no longer in inventory) and toll of goods sold is increased by $iii,000.

Table 1.4 Accounts Used to Record Product Costs

| Account Name | Clarification | Financial Statement |

|---|---|---|

| Raw materials inventory | Cost of unused production materials | Balance sheet (asset) |

| Work-in-procedure inventory | Cost of incomplete products | Balance sail (asset) |

| Finished goods inventory | Cost of completed products not even so sold | Balance sheet (asset) |

| Cost of goods sold | Cost of products sold | Income statement (expense) |

Figure 1.vi Menses of Production Costs through Balance Sheet and Income Statement Accounts

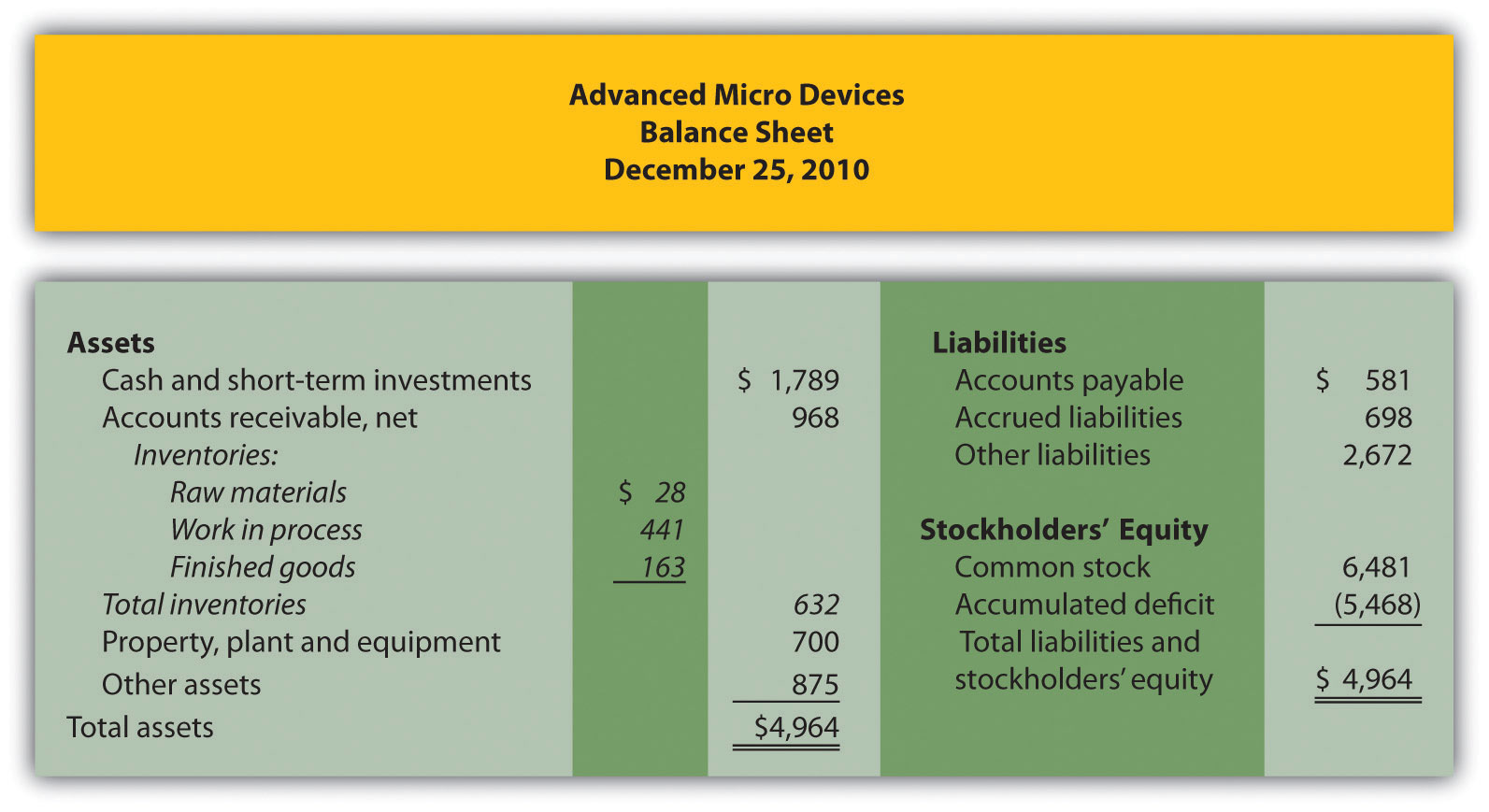

Business in Action 1.vii

Presentation of Product Costs at Advanced Micro Devices

Avant-garde Micro Devices (AMD), a producer of microprocessors and flash memory devices for personal and networked computers, has annual revenues of $6,500,000,000. A summarized version of AMD's rest sheet appears every bit follows (all amounts are in millions). Notice that three inventory accounts, totaling $632,000,000, support the total inventory corporeality that appears in the asset section of the balance canvas. The raw materials inventory account ($28,000,000) is used to tape the cost of materials non notwithstanding put into production. The work-in-process inventory business relationship ($441,000,000) is used to record costs associated with microprocessors and flash memory devices in the production procedure that are not still consummate. The finished goods inventory business relationship ($163,000,000) is used to record the product costs associated with AMD's products that are completed and ready to sell.

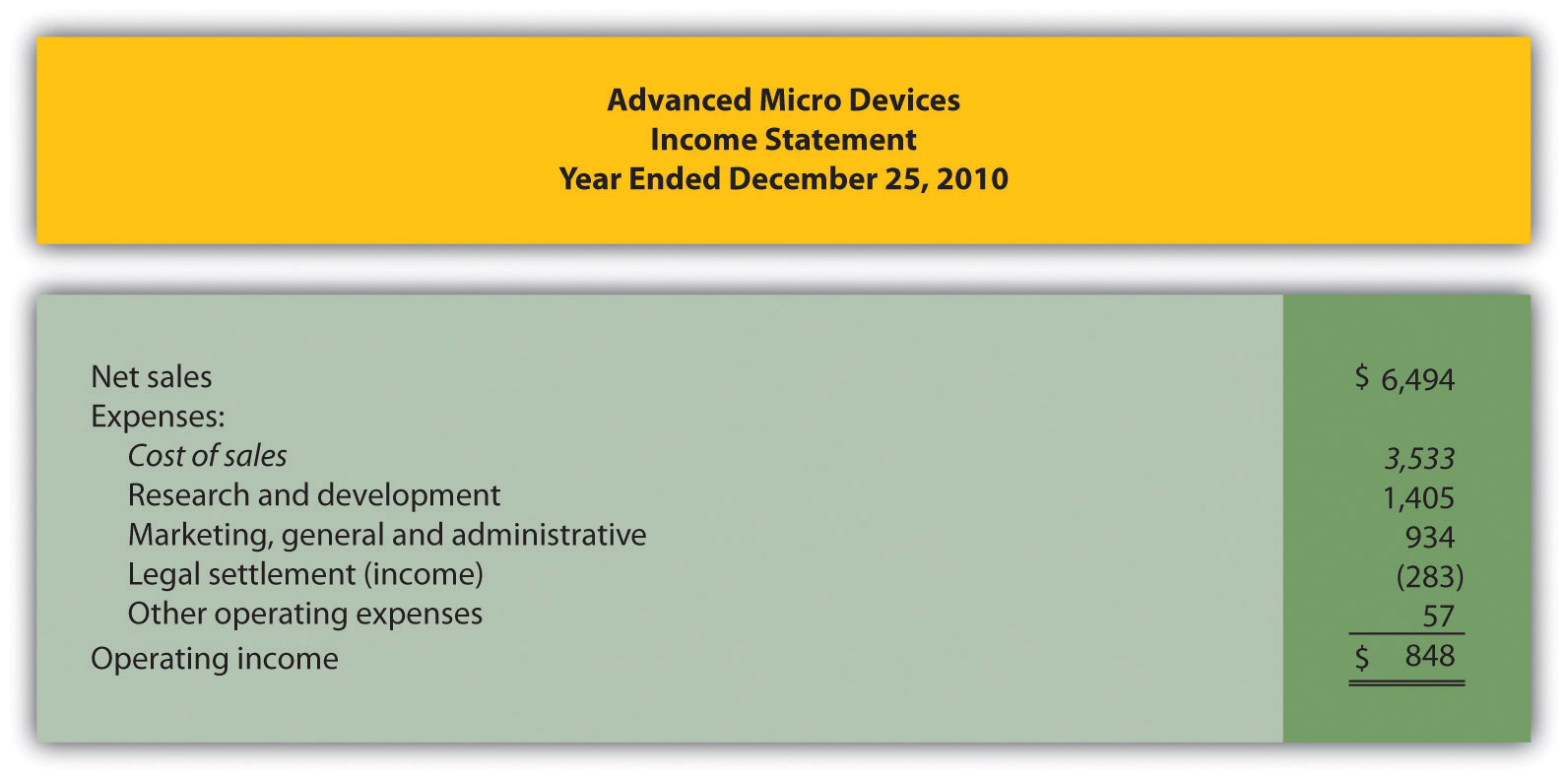

When AMD sells finished goods, the cost of these appurtenances is transferred out of finished appurtenances inventory into the cost of goods sold account, which this company calls cost of sales, as many companies do. The operating portion of AMD's income argument follows—again, all amounts are in millions. Notice that price of sales appears below cyberspace sales and above all other operating expenses.

Source: Advanced Micro Devices, "Avant-garde Micro Devices 2010 Annual Report," http://www.amd.com.

Key Takeaway

- The raw materials inventory account is used to record the price of materials not all the same put into product. The piece of work-in-procedure inventory account is used to tape the toll of products that are in production but that are non all the same complete. The finished appurtenances inventory account is used to record the costs of products that are complete and prepare to sell. These three inventory accounts are assets accounts that announced on the rest canvas. The costs of completed goods that are sold are recorded in the cost of goods sold business relationship. This account appears on the income statement every bit an expense.

Review Problem i.7

Lucifer each of the following accounts with the appropriate clarification that follows.

- _____ Raw materials inventory

- _____ Work-in-process inventory

- _____ Finished appurtenances inventory

- _____ Cost of appurtenances sold

- Used to tape product costs of appurtenances that are completed and gear up to sell

- Used to record production costs of appurtenances that take been sold

- Used to record product costs of goods that are still in production

- Used to tape the cost of materials not yet put into production

Solutions to Review Problem i.7

| Raw materials inventory | 4. Used to tape toll of materials not yet put into production. |

| Work-in-process inventory | 3. Used to record product costs associated with incomplete appurtenances in the production process. |

| Finished goods inventory | i. Used to record product costs associated with goods that are completed and ready to sell. |

| Cost of appurtenances sold | ii. Used to record production costs associated with goods that are sold. |

Which Of The Following Accounts Does A Manufacturing Company, But Not A Service Company, Have?,

Source: https://saylordotorg.github.io/text_managerial-accounting/s05-07-how-product-costs-flow-through.html

Posted by: browncombou.blogspot.com

0 Response to "Which Of The Following Accounts Does A Manufacturing Company, But Not A Service Company, Have?"

Post a Comment